Read the latest FinTech press releases and you might assume quantitative funds are already rebalancing live institutional portfolios on fault-tolerant quantum mainframes. The academic literature and industry reality tell a different story.

Nobody is running production-scale quantum portfolio optimization today in a way that outright defeats state-of-the-art classical methods on massive, real-world datasets. However, assuming you can wait another five years before building internal capabilities is a dangerous miscalculation. Your classical solvers are already maxing out.

For decades, the Markowitz mean-variance model has been the gold standard. With a small asset universe and clean assumptions, classical convex optimization works beautifully. The moment you layer in real-world friction like transaction costs, cardinality bounds, minimum holding periods, ESG constraints, and dynamic risk factors, the problem mutates into a mixed-integer quadratic program. It becomes strictly NP-hard.

Classical solvers are forced into relying on greedy selection, genetic algorithms, and metaheuristics to untangle the combinatorial explosion. You are leaving basis points on the table simply because the raw computational power to find true global optimums across high-dimensional, constrained datasets does not exist classically.

The Operational Friction Point Nobody Mentions on Stage

Moving these complex optimizations to quantum hardware requires reformulating continuous portfolio tasks into discrete frameworks. This is most commonly done as a Quadratic Unconstrained Binary Optimization (QUBO) problem. From there, variational algorithms like QAOA take over. Recent hybrid models, such as two-step QAOA variants, show immense theoretical promise for handling stock selection and risk assessment simultaneously.

There is a major bottleneck rarely discussed at conferences, and that is discretization. If you want to encode a continuous asset allocation, for example, investing 14.5% of your capital into a specific asset, you must translate that weight into a binary string. This requires massive qubit overhead. The higher the precision you demand, the more binary variables you need per asset. This drastically inflates the QUBO matrix. Because current gate-based systems and annealers are constrained by noise and connectivity, we are strictly in the Experimental Utility phase. We are proving the math and mapping the Hamiltonians, but we haven't yet crossed the threshold where quantum price-to-performance beats high-end classical mixed-integer solvers for large-scale portfolios.

Why Elite Quants Aren't Waiting for Fault Tolerance

If the hardware isn’t yielding production-level ROI this quarter, you have to ask why top-tier financial R&D teams are heavily investing right now. The reality is that Quantum Readiness cannot be bought off the shelf the day a logical qubit is announced.

It takes years to train quantitative researchers to abandon purely sequential logic and start thinking in state spaces, interference patterns, and variational circuits. Translating bespoke financial constraints into Hamiltonians is a completely new discipline. The institutions securing a competitive advantage are the ones actively building their internal modeling frameworks today. When devices finally cross key error and scale thresholds, these teams will possess deployable, proprietary IP. Their competitors will be left scrambling to read whitepapers.

Escaping Integration Drag to Benchmark Actual ROI

The immediate hurdle for FinTech VPs isn't getting hyperscaler access. Every major cloud provider will hand you an SDK and a dashboard. The real roadblock is the deployment cycle. Building the infrastructure to test a proprietary optimization model across annealers, trapped ions, and superconducting qubits while managing data pipelines and calibration drift is an operational nightmare. That is where internal R&D stalls.

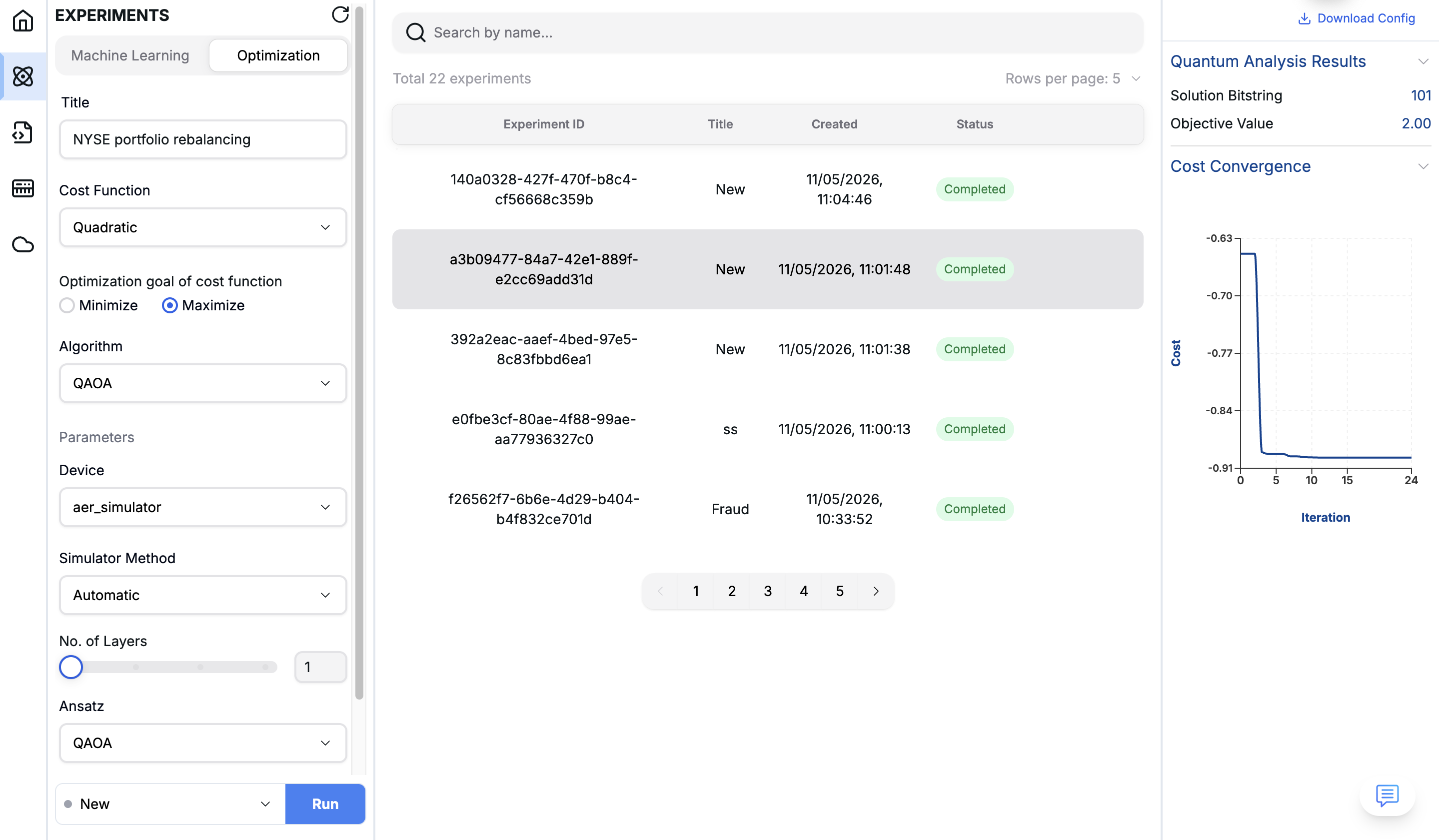

Portfolio Balancing using Bloq

This is exactly why we built Bloq Quantum. We engineered a seamless data-to-deployment ecosystem designed to give your team 10X faster development cycles by eliminating the integration drag between your data and the underlying backends. When your quants struggle to map complex financial constraints, our Optimization Module provides pre-built QUBO pipelines and encoders to handle the heavy lifting of discretization.

Teams can prototype algorithms in our Editor Module (a hybrid Jupyter/GPU workflow) and instantly route experiments across diverse hardware like IBM, Quantum Rings, Qonfluence, and high-performance simulators.

You don't need full fault-tolerance to start. You need an environment that gets your models out of the lab and into empirical, business-case benchmarking on your own proprietary data.

References

- Buonaiuto, G., Gargiulo, F., De Pietro, G., Esposito, M., & Pota, M. (2023). Best practices for portfolio optimization by quantum computing, experimented on real quantum devices. Scientific Reports, 13, 19961.

- Egger, D. J., Gambella, C., Mareček, J., McFaddin, S., Mevissen, M., Raymond, R., Simonetto, A., Woerner, S., & Yndurain, E. (2020). Quantum Computing for Finance: State of the Art and Future Prospects. IEEE Transactions on Quantum Engineering (preprint version arXiv:2006.14510).

- Gondauri, D. (2026). P vs NP Problem in Portfolio Optimization: Integrating the Markowitz–CAPM Framework with Cardinality Constraints and Black–Scholes Derivative Pricing.

- Herman, D., Googin, C., Liu, X., Sun, Y., Galda, A., Safro, I., Pistoia, M., & Alexeev, Y. (2023). Quantum computing for finance. Nature Reviews Physics, 5, 450–469.

- Lee, W. B. (2026). Practical Applications of Quantum Computing in Finance: Mathematical Foundations and Deployment Challenges. Quantum Reports (MDPI, in press).

- Quinton, F. A., Myhr, P. A. S., Barani, M., del Granado, P. C., & Zhang, H. (2025). Quantum annealing applications, challenges and limitations for optimisation problems compared to classical solvers. Scientific Reports, 15, 12733.

- Wu, B., & Wang, L. (n.d.). A Two-Step Quantum Approximate Optimization Algorithm for Portfolio Optimization and Risk Assessment. Quantum Reports.

- Zhang, Y., Leung, T., & Aravkin, A. (2019). A Relaxed Optimization Approach for Cardinality-Constrained Portfolios. European Control Conference (ECC), 2885–2892.

- "Quantum Portfolio Optimization: An Extensive Benchmark." (2025). arXiv:2509.17876

Frequently Asked Questions

Is quantum computing currently being used for live portfolio optimization?

No. The industry is currently in the "Experimental Utility" phase. While algorithms like QAOA are showing theoretical promise, current hardware limitations (noise and qubit counts) prevent them from outperforming classical solvers on full-scale, real-world financial datasets.

What is the biggest technical challenge in quantum portfolio optimization?

A major bottleneck is discretization. Translating continuous asset weights (percentages) into binary strings for quantum processing (via QUBO models) requires a significant amount of qubits to maintain accuracy. This inflates the complexity of the problem beyond what current NISQ devices can comfortably handle.

If quantum isn't production-ready, why should our FinTech R&D team invest in it now?

Quantum algorithms require a fundamental shift in how quantitative problems are formulated. The learning curve is steep. Teams that build internal expertise, map their specific financial constraints to quantum models, and achieve "Quantum Readiness" now will capture the immediate competitive advantage when hardware matures.

How does Bloq Quantum accelerate our quantum R&D pipeline?

Bloq Quantum provides an enterprise-grade "data-to-deployment" ecosystem. Instead of wasting months configuring cloud environments and translating classical data, your team can use our platform to test algorithmic frameworks 10x faster across diverse hardware backends (IBM, Quantum Rings, Qonfluence) and high-performance simulators.